Jan 27, 2020 / Money Tips

Games are fun. Games with your money are not. Many big banks have a whole litany of ways of playing games with your money, but the end goal is usually to keep your money from you, while taking a little bit for themselves. This game of keep-away often gets disguised as a “fee,” which can vary from bank to bank, but there are several that standout as mainstays, including overdraft, maintenance, and minimum balance fees.

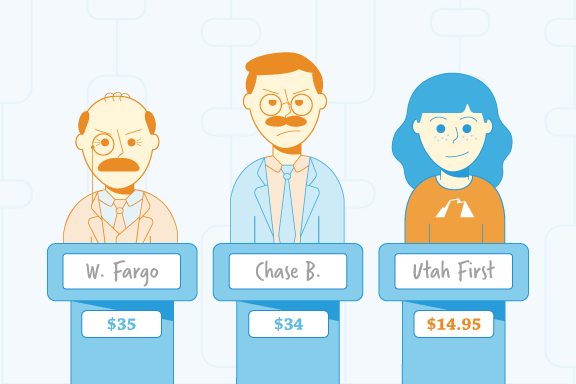

On the surface, overdraft fees are completely understandable. Your bank is covering for you and helping you avoid the embarrassment and hassle of a declined transaction. But what’s not understandable is being overcharged for overdraft. Big banks usually charge between $30 to $35 for overdraft, which can feel less like a courtesy and more like getting kicked while you’re down. Credit unions, on the other hand, usually offer much lower overdraft fees because they aren’t in the business of making money off their members. In fact, Utah First boasts the lowest overdraft protection in Utah at just $14.95 (almost $20 cheaper than the median fee of most big banks).

Another game big banks love to play with your money is charging you for depositing money with them. These charges take the form of maintenance fees and can run between $10 and $12 each month at most major banks, and more than $100 a year. It does take work to maintain an account and keep your money safe, but once again these fees should be minimal. And you should have the option to avoid maintenance fees altogether if you so choose. As you research accounts, ask about maintenance fees and be on the lookout for hidden fees buried in the fine print of your contract. Utah First offers both personal and business accounts with no monthly maintenance fees, giving you the freedom to choose your account style.

Minimum balance fees are a big bank’s way of penalizing you for using more of your money than it wants you to. Minimum balances usually hover around $100, and banks love to slap you with a fee for dipping below this limit. Avoid minimum balance fees by either watching your spending carefully or avoiding opening an account with minimum balance requirements in the first place. At Utah First, you can choose between a Dividend Checking Account, a Personal E-Checking Account, and a Free Checking Account without having to worry about minimum balance requirements or minimum balance fees.

Keep in mind that while all banks have fees, they should never cross the line from helpful service to playing games with your money. If you feel your bank is playing games with your money, stop by a Utah First branch to learn more about how we can save you money.

Sep 17, 2025 / Checking

The Benefits of Opening a Checking Account With a Credit Union vs. a Big Bank

May 27, 2022 / Money Tips

How to Choose the Right Checking Account

Aug 31, 2021 / Local Utah

Finding the Right Fit with Your Financial Institution